The global significance of the July 4th, 2024 election, in which the British Conservative Party suffered its greatest loss in its 190-year history, marks the symbolic death of the neo-liberal economic policies that British Prime Minister Margaret Thatcher and U.S. President Ronald Reagan globalized over 40 years ago.

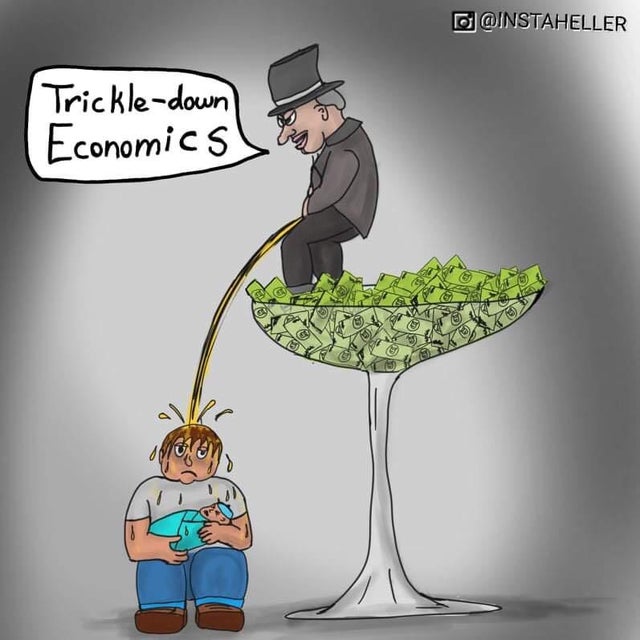

Initially termed Neoconservative or neoclassical economics, these policies essentially negated the social contract between governments and the governed, shifting social responsibilities to free-market principles. This shift resulted in widespread poverty, sociopolitical destabilization, and the rise of money politics devoid of ideology worldwide.

In response to the 1929 Great Depression, economists like John Maynard Keynes advocated for government intervention to stimulate the economy, even if it required operating a deficit budget. Keynes argued that it was the government’s social responsibility to provide employment, alleviate poverty, and support businesses. In 1933, U.S. President Franklin D. Roosevelt introduced the ‘New Deal’ to combat the depression by strengthening the financial system and commissioning large public infrastructure projects, which provided jobs and stimulated the consumer market. Although these efforts temporarily halted the depression, it was the extensive military spending during World War II that ultimately ended it.

The Keynesian model, which promoted government investment in social services even with budget deficits, was widely adopted until the oil crisis of the 1970s. The British Fabian Society spread these economic ideas to leaders of newly independent nations, including Nigeria’s Obafemi Awolowo, India’s Jawaharlal Nehru, Pakistan’s Muhammad Ali Jinnah, Singapore’s Lee Kuan Yew, and Michel Aflaq, the founder of the Ba’athist movement in the Arab world.

However, classical economists pushed back against Keynesian economics, particularly its advocacy for government interventions. They ignored that the West was engaging in “military Keynesianism,” where government investment in military-related industries like automobiles, aircraft, and computers stimulated the economy. The tide turned when Milton Friedman of the Chicago School of Economics won the Nobel Prize in Economics in 1974, leading to the adoption and globalization of neoclassical economic theories by the U.S. Republican government and Bretton Woods institutions.

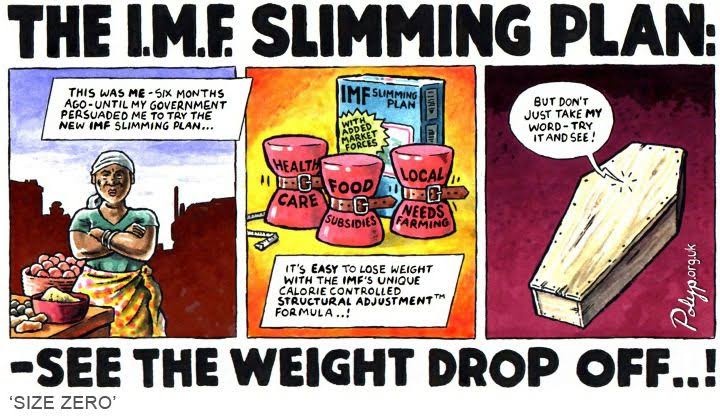

While there was a brief pause during President Gerald Ford’s administration in 1977, British Prime Minister Margaret Thatcher, who came to power in 1979, reignited these policies. When President Ronald Reagan assumed office in 1981, the IMF and World Bank imposed these policies as structural adjustment programs on nations struggling with the double impact of the global fuel crisis and falling commodity prices, especially in Sub-Saharan Africa and South America. These policies were imposed uniformly, regardless of each country’s specific conditions or developmental stage.

In the 1960s, Black African nations had adopted social welfarism and were on par with, or even wealthier than, East Asian nations. However, IMF and World Bank policies, which pushed for the withdrawal of subsidies from education, food, health, and other services, and offered loans that were not directed towards these critical sectors, led to economic collapse in Black African countries. Poverty increased exponentially, while East Asian nations, which did not adopt these policies, experienced rapid growth.

Neo-Conservative economic theories narrowed the political space for alternatives, forcing even liberal leaders like President Bill Clinton and Prime Minister Tony Blair to adopt them, transforming them into neo-liberal economic policies. In Black Africa and South America, political leaders lacked the power to resist the economic tyranny imposed by the IMF and World Bank. Ideological politics became obsolete as leaders like Kenneth Kaunda realized that the international financial system could oust any leader through financial pressure, leading to infamous IMF riots.

Starting in 1999, China, which had avoided Western financial institutions, began investing in Africa, opening mines and industries closed by IMF policies. This investment marked a new dawn for Africa, leading to the “Africa is Rising” narrative. However, the 2008 global economic crash, triggered by subprime mortgages that had replaced government social housing programs, exposed the flaws of neo-liberal economics. The idea that everyone could own a home through free-market principles had been a key selling point of these policies, but the collapse of the subprime mortgage market debunked this myth.

The British electorate, disillusioned by 12 years of stagnant wages and a destabilized labor market under Conservative rule, ousted the Tories. Neo-Conservative policies had also embedded ethnic discrimination, with Black Diasporans arguing that the policies targeted their employment opportunities in large government institutions under the guise of rationalization and commercialization. Social welfare benefits for Black and other non-White ethnic groups were also reduced. Instead of admitting the failure of their policies, the British Conservatives engaged in divisive politics, blaming immigrants and pushing for Brexit, which further damaged the economy. Meanwhile, Continental Europe, which did not fully embrace neo-liberal policies, saw growth in infrastructure, prosperity, and quality of life indices.

Unlike Western nations with stable democracies, where Neo-Conservative/Neo-liberal politicians could be voted out, Africans often have no choice but to revolt. Recently in Kenya, youths rose up against IMF-induced tax increases by President Ruto, who is struggling to maintain power despite reversing his tax hike proposals, sacking his cabinet, and cutting political salaries.

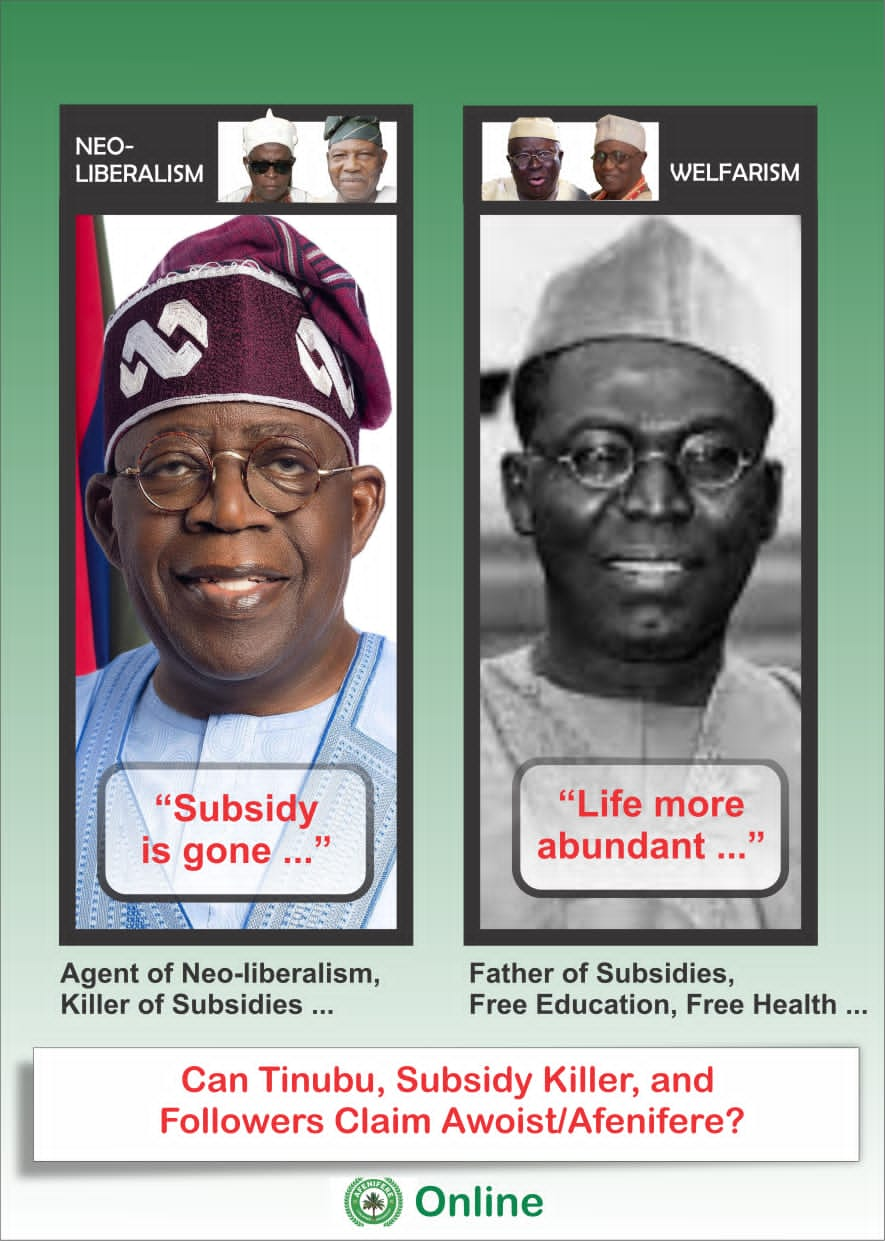

In Nigeria, President Bola Tinubu tapped into neo-liberal practices by alleging that the “Hunger Protests” were tribally and politically motivated, while relying on tribal loyalty to avoid participating in the protests. Regardless of what African leaders do, if they do not abandon neo-liberal economics and instead use budget deficits to initiate large-scale employment and infrastructure programs to close the 40-year gap, they will face revolutions worse than the Haitian Revolution. Tinubu, who originally came from Awolowo’s social welfarist group Afenifere, is living on borrowed time. If he does not retrace his steps to Awoism and initiate a Roosevelt-style New Deal, history will judge him harshly as his neo-liberal policies lead to political implosion, potentially threatening Nigeria’s corporate existence. Like the British, the people will eventually reject divisive ethnic tactics and rise up for a new social contract that emphasizes government responsibility in making life more abundant through subsidies and investment in employment, education, and health, rather than relying on free-market principles